Payment methods in Africa - statistics & facts

The digital payments market in Africa has boomed in recent years, showing few signs of slowing down; the market continues to grow. Emerging trends in mobile money have been a primary driver of this growth.

In 2025, Sub-Saharan Africa processed 92 billion mobile money transactions in 2025, at a combined value of 1.4 trillion U.S. dollars, roughly 67 percent of global transaction value. However, the pace of digital payment adoption in Africa has been uneven, with usage rates varying from country to country. As of 2025, almost 70 percent of Senegalese people had made a digital payment in the previous year. This is a stark contrast to Niger, where less than 10 percent of people had made a digital payment in the past year.

IPS Infrastructure Expanding Across the Continent

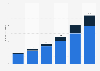

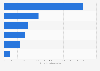

Active instant payment systems (IPS) began to gain traction on the continent during 2007. As of late 2025, a large portion of countries in Africa operated at least one IPS. Nigeria operates three IPS, while Egypt, Ghana, Kenya, Morocco, South Africa, and Tanzania each run two, bringing the total number of IPS in Africa to 33. The IPS have gained popularity in recent years, seen through the rapid uptick in usage. IPS transaction volume in Africa hit 65.6 billion in 2024, up from 14.1 billion in 2019, a more than fourfold increase in five years. Payments also dominate Africa's fintech ecosystem more broadly. At 346 active platforms recorded in 2025, it is the largest product category among African fintech offerings, well ahead of lending and crowdfunding at 207 companies.

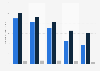

Security Concerns and Outages Slow Cash-First User Conversion

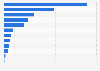

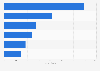

The barriers keeping cash-dependent users off digital platforms are specific and measurable. Fraud and security concerns ranked as the top obstacle among cash-first IPS users. Network and platform outages were the second most prominent obstacles for cash-based users to make the switch to IPS. On the merchant side, the friction runs just as deep; customers' continued preference for cash was the primary constraint outlined by merchants when adopting IPS. A need for more training ranked as the second most common constraint. These friction points operate on both sides of the transaction and will not be resolved without deliberate action by providers and regulators alike.

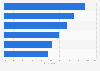

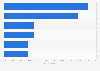

Cross-Domain IPS Lead Africa's Growing Transaction Value

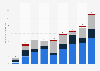

Cross-domain IPS accounted for the largest portion of IPS total transactions, reaching roughly 1.3 trillion U.S. dollars. Mobile money transactions ranked second, having accounted for 535 billion U.S. dollars, and bank-based systems made up the smallest portion, accounting for 147 billion U.S. dollars. When reviewing transactions by volume, however, mobile money dominated; of the 65.6 billion IPS transactions processed across the continent in 2024, 50.3 billion moved through mobile money IPS systems, compared to 13.6 billion for cross-domain and just 700 million for bank IPS. Together, these figures show a market split between high-value cross-domain flows and high-frequency mobile money transactions.

Wallets and Fintech Revenue Point to Structural Shift by 2030

Africa's payment mix is set to look substantially different by the end of the decade. Digital and mobile wallets accounted for 27 percent of POS transaction value in the Middle East and Africa in 2025 and are forecast to reach 35 percent by 2030, overtaking debit cards as the leading point of sales (POS) payment method in the Middle East and Africa. Africa has also been projected to record the strongest fintech revenue growth by region globally between 2021 and 2030, with revenue expected to reach 65 billion U.S. dollars, a thirteenfold increase. The structural transformation already visible in IPS volumes and mobile money adoption is still in its early stages, and the continent's unresolved barriers around security, outages, and fees are the remaining work that will determine how close the 2030 numbers come to the top of the forecast range.