Container freight rates - statistics & facts

From pandemic disturbances to Red Sea tensions, the story of container freight rates in the 2020s is one of fragility. In mid-2024, rates rose to multi-year highs, pushed by a confluence of global shocks such as shipping lane disruptions, port congestion, and regulatory pressures. By July 2025, rates had decreased but remained unpredictable, underscoring persistent challenges in global logistics and supply chain resilience. Based on aggregated data across all trade lanes, shipping a 40-foot container at the beginning of July 2025 cost approximately 2,812 U.S. dollars – less than half the peak of 5,901 dollars recorded one year earlier.

The last comparable volatility occurred during the 2008 global financial crisis. While the underlying causes differ, both episodes exposed the interconnected and vulnerable nature of the global supply chain.

In 2024, a major disruptor was vessel rerouting due to Houthi attacks on commercial ships in the Red Sea. With key shipping lanes becoming unsafe, carriers diverted ships around the Cape of Good Hope instead of through the Suez Canal, lengthening journey times and tightening supply. Coupled with port congestion and blank sailings, this pushed rates to record highs.

A May 2025 United States-Houthi ceasefire caused rates to fall and briefly raised hopes for a widespread return of container shipping in the Red Sea, but it was violated after a month. Despite easing prices, market volatility persists amid ongoing rerouting and tariff uncertainties. For example, in June 2025, a pause in the U.S.–China tariff war triggered a temporary spike in Asia-North America rates.

While manufacturers and consumers bear the increasing costs of shipping, carriers saw strong profits in late 2024, with average operating margins exceeding 25 percent – up from -3.8 percent one year earlier. Many are investing these profits in new ships and containers, although new vessels will take years to enter service.

While freight rates have retreated from their 2024 highs, the market continues to face pressures from geopolitical instability, climate-related disruptions, and shifting trade policies. As decarbonization mandates and supply chain regionalization reshape the market, the industry’s future will depend not only on market trends, but also on carriers’ resilience and adaptability.

The last comparable volatility occurred during the 2008 global financial crisis. While the underlying causes differ, both episodes exposed the interconnected and vulnerable nature of the global supply chain.

Freight rates descend following turbulent 2024

The global supply chain is a fragile and interconnected ecosystem made up of several interdependent nodes. The early 2020s saw container shipping hit by successive shocks – from the COVID-19 pandemic to geopolitical tensions, port congestion, container shortages, rising fuel prices, and new environmental regulations.In 2024, a major disruptor was vessel rerouting due to Houthi attacks on commercial ships in the Red Sea. With key shipping lanes becoming unsafe, carriers diverted ships around the Cape of Good Hope instead of through the Suez Canal, lengthening journey times and tightening supply. Coupled with port congestion and blank sailings, this pushed rates to record highs.

A May 2025 United States-Houthi ceasefire caused rates to fall and briefly raised hopes for a widespread return of container shipping in the Red Sea, but it was violated after a month. Despite easing prices, market volatility persists amid ongoing rerouting and tariff uncertainties. For example, in June 2025, a pause in the U.S.–China tariff war triggered a temporary spike in Asia-North America rates.

Carrier strategies diverge amid fluctuating rates

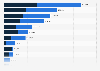

The global container shipping industry is dominated by a handful of players – including Maersk, MSC, and CMA CGM – who together control over 85 percent of global volume, largely via alliances such as 2M, Ocean Alliance, and THE Alliance. In 2024, Maersk reported an average rate of 2,698 dollars, well above Hapag Lloyd’s 1,492 dollars, reflecting differences in routes, customer bases, and strategies. For instance, Maersk invested in end-to-end logistics and warehousing, aiming to become a full-service logistics provider. In contrast, MSC has focused on rapid fleet expansion, overtaking Maersk as the world’s largest container line by capacity.While manufacturers and consumers bear the increasing costs of shipping, carriers saw strong profits in late 2024, with average operating margins exceeding 25 percent – up from -3.8 percent one year earlier. Many are investing these profits in new ships and containers, although new vessels will take years to enter service.

While freight rates have retreated from their 2024 highs, the market continues to face pressures from geopolitical instability, climate-related disruptions, and shifting trade policies. As decarbonization mandates and supply chain regionalization reshape the market, the industry’s future will depend not only on market trends, but also on carriers’ resilience and adaptability.